A credit score is your credit report distilled down to a single number. The intent is to predict your credit worthiness based solely on the information contained in your credit report. The most popular credit score is the FICO Score from the Fair Isaac Corporation.

Although the exact method for calculating the FICO Score is kept secret, the basic recipe for the score is taken from 5 key factors from your credit history.

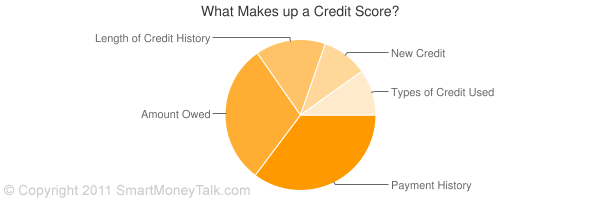

- Payment history (35%)

- Amount owed (30%)

- Length of credit history (15%)

- Amount of new credit (10%)

- Types of credit used (10%)

1. Payment history

At 35% of your credit score, your payment history is the most important information used to calculate your score.

These factors increase your score:

- Pay each account (at least the minimum amount) on time.

- If you’ve had payment problems, your score will increase as the number of months since the last problem increases.

- The more credit accounts that are paid in full (car loans, mortgages, etc), the higher your score.

These factors decrease your score:

- The more records of payment problems, the lower your score. Examples include paying your bills late, accounts sent to a collections agency, bankruptcy, judgements, liens, and wage garnishment.

- The amount of time each account is late – the longer you wait to pay, the more your credit score goes down.

- The number if past due accounts on record – the more accounts you pay late or don’t pay at all, the lower your credit score.

2. Amount owed

The amounts you owe on your credit accounts make up the next 30% of your score. You can improve your credit score by:

- Keep your credit utilization percentage low. The lower your credit utilization percentage, the higher your credit score.

credit utilization percent = total credit used / total credit limits

- Account balances – the fewer accounts that have ongoing balances, the higher your score.

3. Length of credit history

The length of your credit history accounts for 15% of your score. The only thing you can do is get credit early, and wait for time to pass. The longer you’ve had accounts open and the longer you’ve had activity on your accounts – the higher your credit score.

4. Amount of new credit

New credit accounts in your credit report account for 10% of your credit score. The more of the following, the lower your score:

- As you open more new credit accounts, your score will decrease. The amount of decrease depends on how many credit accounts you have. If you have many older accounts and only a few new accounts, this factor should not affect your score too much.

- The more credit inquiries have on your credit report in the past year, the lower your score.

5. Types of credit used

The final factor – the types of credit used – accounts for the last 10% of your score. In general, you want a variety of types of credit such as: credit cards, installment loans, a mortgage, retail accounts, etc. The more variety, the higher your score.

How can I find out my credit score?

- Starting July 21, 2011, if you are denied a loan or credit application, you can get a free credit score from the company that denied you credit.

- If you haven’t been denied a loan or credit application, you can always go to the source and get your FICO score directly from the Fair Isaac Corporation (the creators of the FICO credit score). It costs $14.95 per month, and gives you the ability to watch out for changes in your score over time.

- An alternative to Fair Isaac’s service is CreditKarma.com. They been written up in the Wall Street Journal, USA Today, and hundreds of other publications. They give you access your TransRisk Score, Auto Insurance score, and VantageScore. The TransRisk Score is calculated by TransUnion–one of the 3 major credit reporting agencies. While it’s not the exact same as the FICO Score, it’s pretty close. You can go to their site to update your scores monthly. This will enable you to monitor changes in your credit, and (best of all) it’s free. To get your scores, sign-up at CreditKarma.com.

Read More

Source: http://www.myfico.com/downloads/files/myfico_uyfs_booklet.pdf

Pingback: What is a good credit score?